A Deep Dive Into Agility Robotics: The Humanoid That Already Has a Job

On Agility's GXO Warehouse work, Specs, BoM and competitors

There’s a moment in every new technology category where the market stops asking “could this work” and starts asking “what’s it worth.” Humanoid robotics hit that moment on June 24, when Agility Robotics announced it’s going public through a merger with Churchill Capital Corp XI, ticker CCXI, at a $2.5 billion pre money valuation.

The combined company will trade as AGLT once the deal closes. For now, exposure means buying the SPAC.

Most of what gets written about humanoid robots right now is theater. A guy in a lab coat shows you a robot folding a towel, followed by a breathless thread about how this changes everything. Tesla’s Optimus has been the loudest example for two years running. On the company’s own Q4 2025 earnings call, Elon Musk admitted the Fremont units exist “primarily for learning, not productive tasks.”

Fine R&D strategy. Not a revenue strategy.

Agility Already Has Customers

Before this SPAC was ever announced, Agility’s robot, Digit, had already moved more than 100,000 totes inside a GXO warehouse doing real, billed, production work. It’s running shifts at Schaeffler, deployed at Toyota Motor Manufacturing Canada, and working inside a Mercado Libre fulfillment center.

This is arguably the humanoid platform with the deepest track record of sustained commercial work today. Figure AI has real deployments too, including a BMW production line, but its footprint is newer and narrower. Boston Dynamics’ Atlas handles structured tasks at Hyundai, but the company has leaned more toward research demonstrations than commercial scale.

So this isn’t a story about whether humanoid robots are coming. They’re already here, doing a narrow set of jobs, in a handful of warehouses. The question is whether Agility turns that early lead into the dominant commercial platform before Tesla’s manufacturing scale, Figure’s capital war chest, or cheap Chinese hardware from Unitree catches up.

The technology argument here is stronger than the financial argument, which is unusual for a SPAC and worth digging into.

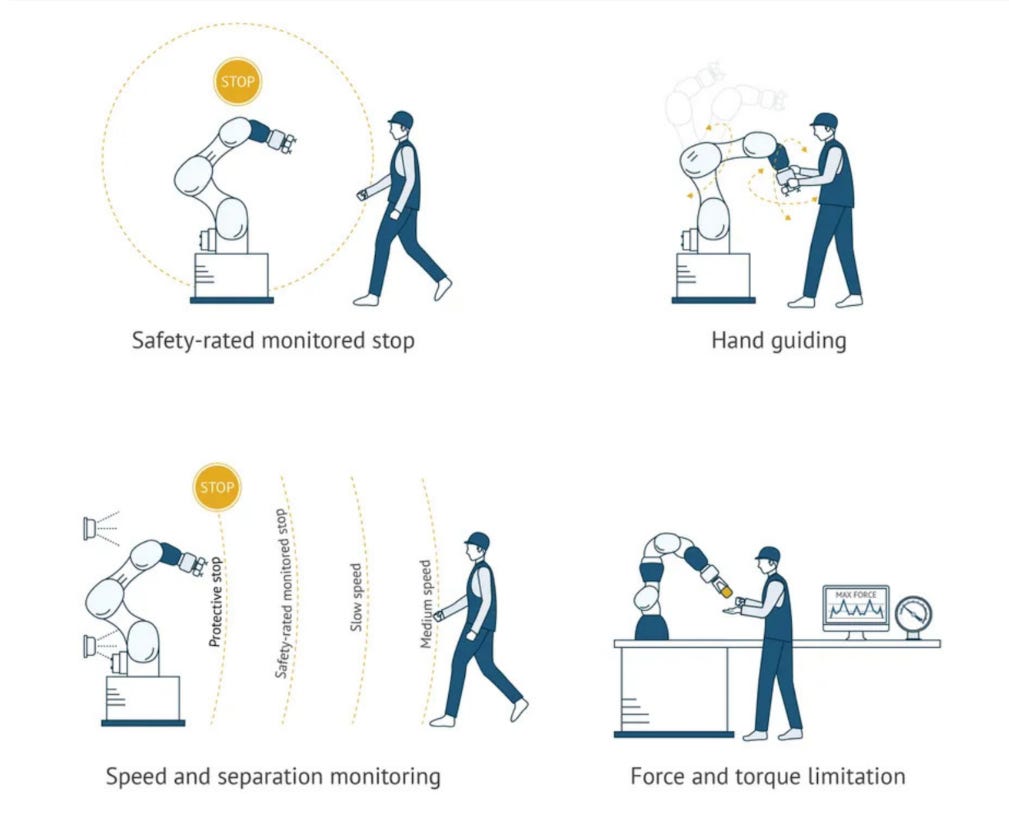

What Cooperative Safety Actually Means

This is the actual engineering unlock that determines whether humanoid robots scale past a few hundred units.

Every humanoid and industrial robot in a warehouse today operates inside a cage, a fenced workcell, or a virtual exclusion zone. The IEC and ISO standards that insurers and OSHA effectively require have no established framework for letting a robot and a person share unstructured space. You can’t put a forty pound humanoid next to someone loading a truck without a certified way to guarantee it won’t hurt them.

That fencing requirement is the single biggest reason robotics adoption in logistics has stayed stuck at a few automated zones inside otherwise human run buildings.

Digit v5 is built specifically to remove that fence. Agility calls this “cooperative safety,” and it’s a specific technical architecture built with NVIDIA. In June, NVIDIA announced Halos for Robotics, its first full stack safety system for physical AI, and Agility is the launch partner, the first company shipping a production humanoid with it built in.

The stack itself: the compute core is NVIDIA’s IGX Thor module, which contains a Functional Safety Island, a dedicated processor running independently from the robot’s main AI brain, rated to IEC 61508 SIL 3, the integrity level used where failure could cause serious injury.

On top sits Halos OS, paired with the Outside In Safety Blueprint, which uses external cameras around a facility to watch for people entering a robot’s working zone and dynamically adjust its behavior rather than just stopping dead or staying caged.

NVIDIA built this by extending more than 18,600 engineering years of autonomous vehicle safety work into a robotics context, the same lineage that underpins self driving car certification. Functional safety for machines moving through unpredictable environments is one of the hardest unsolved problems in applied AI, and NVIDIA has already spent a decade solving a version of it for cars.

Agility has also joined NVIDIA’s Halos AI Systems Inspection Lab, an accredited inspection body recognized by TUV Rheinland, TUV SUD, UL Solutions, exida, SGS, and CertX, which pre certifies robotics safety systems before full third party certification under IEC 61508, ISO 13849, and ISO/IEC TR 5469. That’s the difference between a company claiming its robot is safe and a company building a paper trail an insurer and a regulator will actually accept.

The Spec Sheet Backs Up the Strategy

Digit v5 stands about five feet nine, lifts up to fifty pounds, which matches OSHA’s recommended maximum for human manual lifting, reaches up to seven point two feet, and runs for up to twenty two hours on a charge.

None of that is flashy next to Boston Dynamics’ Atlas, which can run, jump, and backflip thanks to its more athletic, research oriented design. But Atlas isn’t trying to work a ten hour shift next to a person loading pallets. Digit is, and every spec on that sheet is tuned for that job rather than a viral video.

This is where I think the market is mispricing the category. Most humanoid narrative gets built around general intelligence, the idea that whichever company trains the smartest foundation model for robot control wins everything. That’s a real axis of competition, Agility cites Google DeepMind as a technology collaborator alongside NVIDIA. But in the next eighteen months, before any of these robots do genuinely general purpose work, the gating factor for revenue is certification and insurance, not intelligence.

A robot that’s less dexterous but certified to work unfenced next to a person today is worth more revenue right now than a brilliant robot that legally has to stay caged. Agility built its v5 platform around winning that narrower, nearer term race, and that’s the correct strategic call for where the market actually is in 2026.

From Pilot to Payroll

Agility sells Digit two ways: outright capital purchase, or a robotics as a service subscription the company says is designed to generate a positive customer return in under a year.

RaaS lowers the barrier for a logistics operator to try a single robot without committing a quarter million dollars up front. It gives Agility recurring revenue instead of a lumpy hardware sale, and it keeps the robot connected to Agility’s fleet management platform, Arc, which runs on Microsoft’s cloud. Every hour Digit works in a real facility feeds data back into training the control software, a flywheel that’s core to how the platform improves rather than waiting for the next hardware generation.

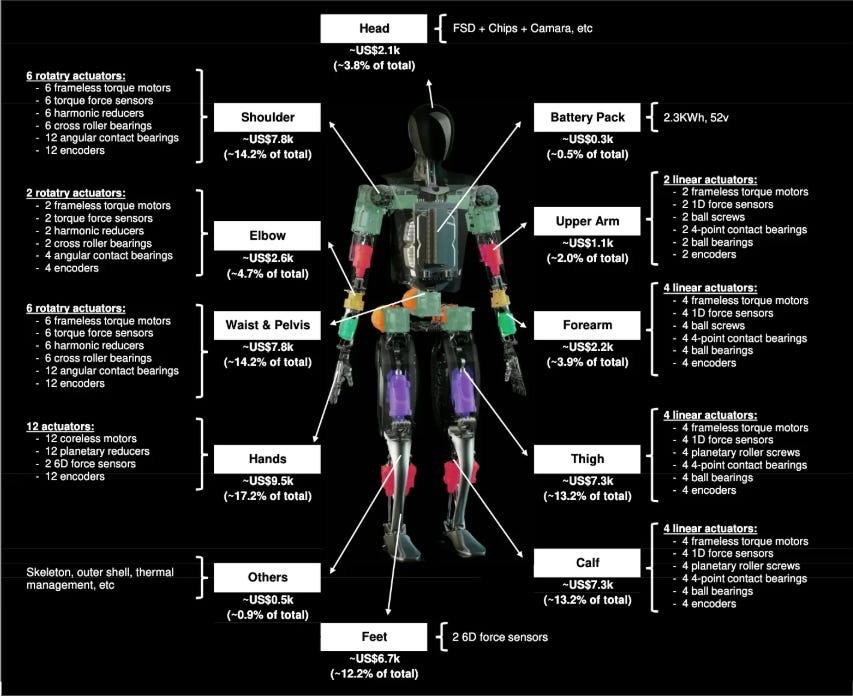

The Bill of Materials Problem

The unit economics question is the bill of materials. Building one Digit v4 costs roughly $125,000 today, a disclosed figure rather than a marketing estimate. At that cost, either model’s economics are tight.

Management’s target is to bring that down toward $30,000 per unit as production scales, a roughly seventy five percent reduction. Aggressive, but not unreasonable, since the playbook is the same one that brought down costs in solar, lithium batteries, and EV drivetrains: more volume through a dedicated factory, vertical integration of expensive subsystems like actuators and sensors, and design simplification as engineers learn what actually breaks in the field.

That’s where RoboFab comes in, Agility’s Salem, Oregon facility with a stated theoretical capacity of 10,000 robots a year once fully ramped. For comparison, Hyundai has committed $26 billion to a new robotics factory targeting 30,000 Atlas units a year, and Tesla is converting Fremont production lines toward Optimus with a reported $20 billion of 2026 capex.

Agility’s manufacturing ambition is smaller in absolute scale, which makes sense for a much smaller company, but the capacity exists today rather than as a future announcement. Foxconn, the world’s largest contract electronics manufacturer, is both leading the PIPE financing in this deal and positioned as the overflow manufacturing partner if Digit v5 orders exceed what RoboFab can build alone.

The Order Book, and Its Fine Print

Agility has disclosed more than $300 million of multi year contracted orders for Digit v5. The fine print matters here: that figure comes overwhelmingly from a single three year contract for 1,000 robots with an undisclosed customer, and the filings state explicitly the $300 million “is not a measure of current period revenue” and depends on hitting contractual milestones.

Real commercial commitment, not booked revenue, with a meaningful chunk resting on one counterparty.

Operating expenses rose from about $71 million in 2024 to roughly $111 million in 2025, with the company burning around $100 million in cash last year. Agility has raised more than $390 million in private equity since its 2015 founding, and this SPAC’s $620 million in expected gross proceeds, including the $200 million Foxconn led PIPE priced at $10 a share, is framed explicitly as the funding round that lets the company fulfill those orders, scale RoboFab, and keep investing rather than running out of runway mid ramp.

The pipeline beyond that headline contract includes more than thirty customers in active discussions, with named relationships at Amazon, GXO, Schaeffler, and Toyota Motor Manufacturing Canada.

Amazon is the one to watch closest. Its Industrial Innovation Fund put $150 million into Agility in 2022, and as the largest logistics operator on the planet, any meaningful expansion of Digit inside actual Amazon fulfillment centers, beyond its current limited presence, would be the single biggest revenue catalyst available. It’s also the single biggest unresolved variable in the case.

Amazon has its own internal robotics division and has shown a willingness to build rather than buy when a technology becomes strategically important, so the relationship cuts both ways: validation of the technology, but also a reminder that the company’s largest potential customer is also a capable potential competitor.

The Crowded Floor

Agility doesn’t win this by default. The competitive set is genuinely strong.

Tesla’s advantage is manufacturing scale and balance sheet. If Optimus’s Gen 3 hands start doing genuinely productive autonomous work at Fremont this year, the milestone the industry is watching for in the back half of 2026, Tesla’s ability to convert existing production lines and its targeted $20,000 to $30,000 unit cost would be hard to match on price.

The counterpoint: Tesla has repeatedly missed its own unit targets, declined to set a new one on its most recent earnings call, and Musk’s own admission about the current fleet’s purpose tells you productive deployment is still mostly ahead of them.

Boston Dynamics, under Hyundai, has the most athletically capable hardware by a wide margin, with Atlas already sequencing car parts inside Hyundai’s own plants and a $26 billion manufacturing commitment behind it. But Atlas is priced as an enterprise grade platform in the $150,000 to $320,000 range by industry estimates, no official price has been published, and Boston Dynamics has historically positioned Atlas more as a research showcase than a mass commercial product.

Figure 02 At Work

Figure AI is the best funded pure play challenger, valued around $39 billion. Its predecessor platform, Figure 02, ran an eleven month production deployment at BMW’s Spartanburg plant and has also had a presence in Amazon warehouses. The newer Figure 03 has since started replacing it at Spartanburg on logistics tasks. Figure is private, so retail investors have no direct way to buy this exposure today, which is part of what makes Agility’s SPAC route interesting: it’s first to the public markets among the serious contenders, by a wide margin.

Then there’s Unitree and the broader Chinese robotics ecosystem, rewriting the price floor for the category. I take this seriously over a three to five year horizon, less so in the next eighteen months, because Unitree’s hardware hasn’t demonstrated the kind of sustained, certified, unfenced industrial deployment Digit already has, and US logistics customers carrying liability exposure won’t deploy uncertified hardware next to their workforce regardless of price. But hardware cost curves move fast, and this could become the more dangerous competitive threat by 2028.

Agility isn’t trying to win on raw athleticism like Atlas, on price like Unitree, or on capital firepower like Tesla or Figure. It’s trying to win on being first to certified, unfenced, real world commercial deployment, and right now, it actually is first.

That lead looks durable for the next twelve to eighteen months, because certification, customer integration, and the operational trust built from 100,000-plus totes moved without incident aren’t things a competitor can announce their way past. Past that window it gets murkier, since every competitor is racing toward the same safety architecture, NVIDIA is selling Halos to all of them, and the moat narrows to execution speed rather than a structural technology gap.

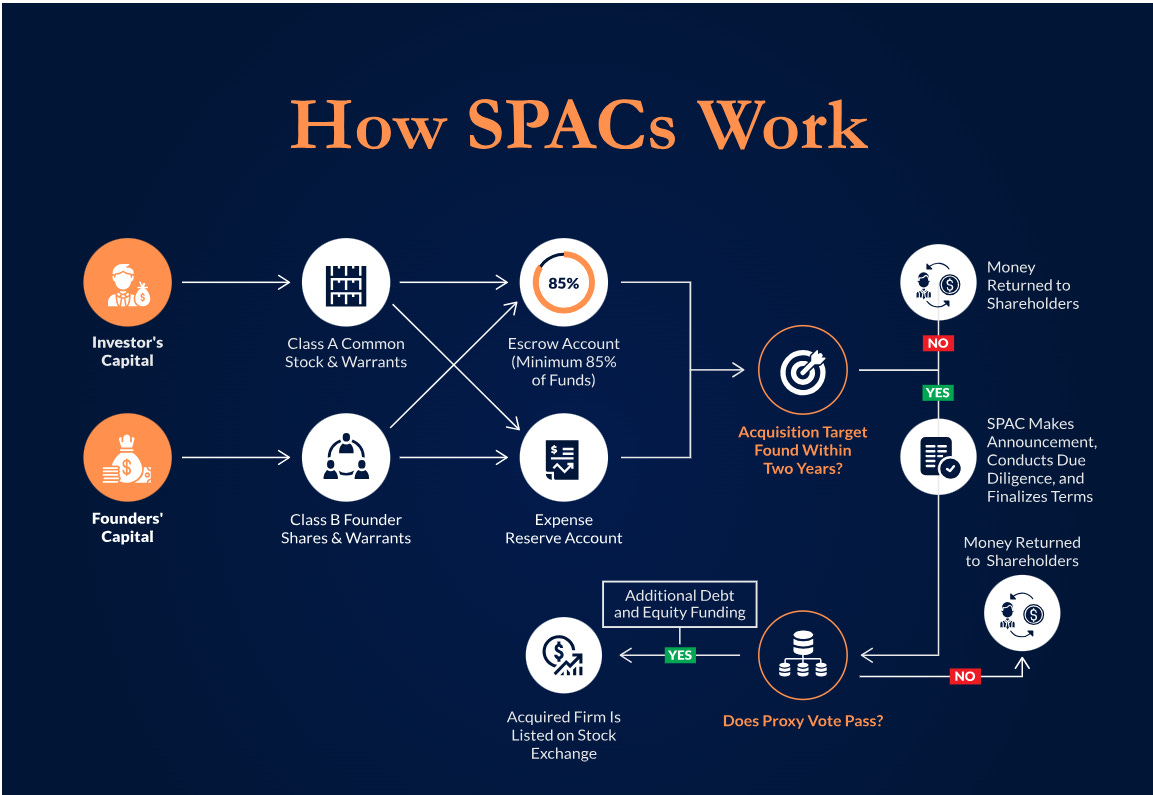

The SPAC Mechanics

CCXI is currently a shell with no operating business, and the stock is effectively an option on the merger closing on the terms announced. The deal requires a Form S-4 registration, SEC review, shareholder votes from both companies, Nasdaq listing approval, and a minimum cash condition of $200 million.

None of that is unusual for a SPAC of this size. One hundred percent of existing Agility shareholders rolling their equity into the deal with a 180 day lockup is a genuinely good alignment signal.

CCXI traded around $10 to $11, basically trust value, right up until the announcement, then jumped double digits and has continued climbing toward the high teens since, trading around $16 to $17 as I write this with the deal still pending close. That’s the market already pricing in real optimism about a transaction that hasn’t closed yet.

I’m not walking through a full DCF here. Agility hasn’t disclosed actual revenue figures, which makes a precise price target more guesswork than analysis at this stage. The more useful exercise right now is understanding the technology and commercial mechanics well enough to know what to watch as real numbers come through the S-4 and subsequent filings.

What I’m Watching

Whether Digit v5’s cooperative safety certification clears third party review on management’s suggested timeline. That’s the unlock for moving Digit into genuinely unstructured shared space at scale, the single biggest lever on total addressable market.

Whether the undisclosed 1,000 unit anchor customer gets named or expands. Right now that’s a concentration risk dressed up as a growth story.

The bill of materials roadmap. The gap between $125,000 today and the $30,000 target is the entire difference between a niche premium product and a platform that can saturate a market management sizes at roughly a trillion dollars across US manufacturing, distribution, and logistics.

And Amazon, closely. That relationship alone could move this story more than every other catalyst combined, in either direction.

Why I’m In

None of this is financial advice, and I’d treat anything priced off Agility’s revenue today with real skepticism, since there effectively isn’t disclosed revenue yet to price off of.

Is this a speculative play? Yes.

But as a bet on which humanoid robotics company is actually closest to doing real, certified, unfenced commercial work at scale, rather than which one has the best demo reel, Agility going public through CCXI gives retail investors their first direct shot at the name with the strongest claim to that title. I’m in, sized modestly given how early this still is, and I’ll follow up once the S-4 drops with actual financial detail to dig into.

If you got here, thanks for reading ❤️

If you’re new, subscribe for more content like this.

-Gabriel